Holding SpaceX Through the IPO: When the 90% Still Lies Ahead

Re-running the Three Futures Test on my own position as the S-1 hits public markets

A continuation of the “Three Possible Futures“ series: this time, applied to my own SpaceX position as it heads to public markets.

This past week, SpaceX filed its S-1 (and had its first successful Starship mission)… and as I worked through the 685-page prospectus (or at least had Claude assist me in doing so), I was pulled back to the piece I wrote almost two years ago, Why Being Late Can Still Mean Capturing 90% of the Upside. At the time, I was reflecting on Starship’s first “Mechzilla” catch and revisiting why I had originally invested in SpaceX… not for Mars, but for the galactic telecom company I believed it was quietly becoming.

That thesis is no longer a private bet. It’s now sitting in audited financials, on its way to what looks likely to be a $1.75 trillion debut on the Nasdaq under SPCX.

And the trade is in front of me.

I came in at a ~$40 billion valuation years ago (thinking it was rather ‘rich’ then), a private placement secured through my network (before all these crazy multi-tier SPVs craze we are seeing around Anthropic et al.), when SpaceX still felt like a difficult deal to access. At today’s secondary marks, I’m sitting on something close to 3,000% on paper. At the IPO target, that’s closer to 43x.

By any disciplined definition, this is a “take some chips off the table” moment.

So I want to think out loud about why I’m leaning to not doing that… also, it should be said that none of this is financial advice. It is a personal reflection on my own position and decision-making. Many of my private placement & angel investments are made with the assumption that they could go to zero and I size them accordingly. As the saying goes, past performance is not indicative of future results.

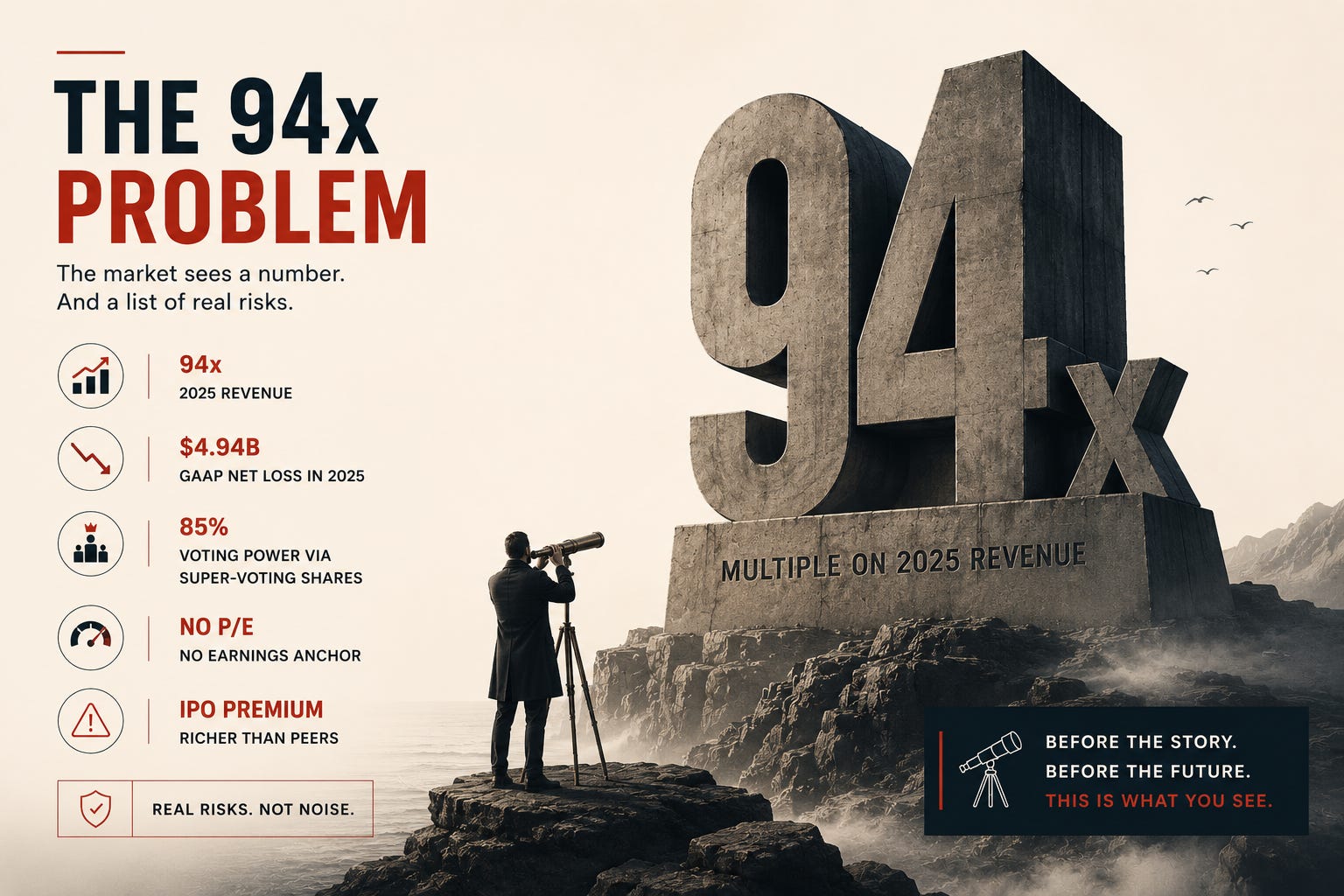

The 94x problem

The headline number that everyone is fixated on is the multiple: 94x 2025 revenue, with a $4.94 billion GAAP net loss in 2025 and a $4.28 billion loss in Q1 2026 alone. Nvidia trades in the single-to-low-double-digit revenue multiples. Tesla sits around 8–10x. Even the most aggressively priced recent IPOs have topped out between 20x and 40x. There is no P/E to anchor to, there are no profits to put a P over. Musk retains 85% of the voting power through a super-voting share class.

This is a real list of risks. I want to take it seriously rather than wave it away.

But the question that actually matters, the one I keep coming back to, is whether the 90% of future value I originally bought into is still ahead, or whether it’s mostly behind me.

After reading the S-1, I believe most of it is still ahead. And that conviction isn’t a feeling, but rather the output of re-running the framework I’ve been writing about: the Three Futures Test.

The multiple, reframed

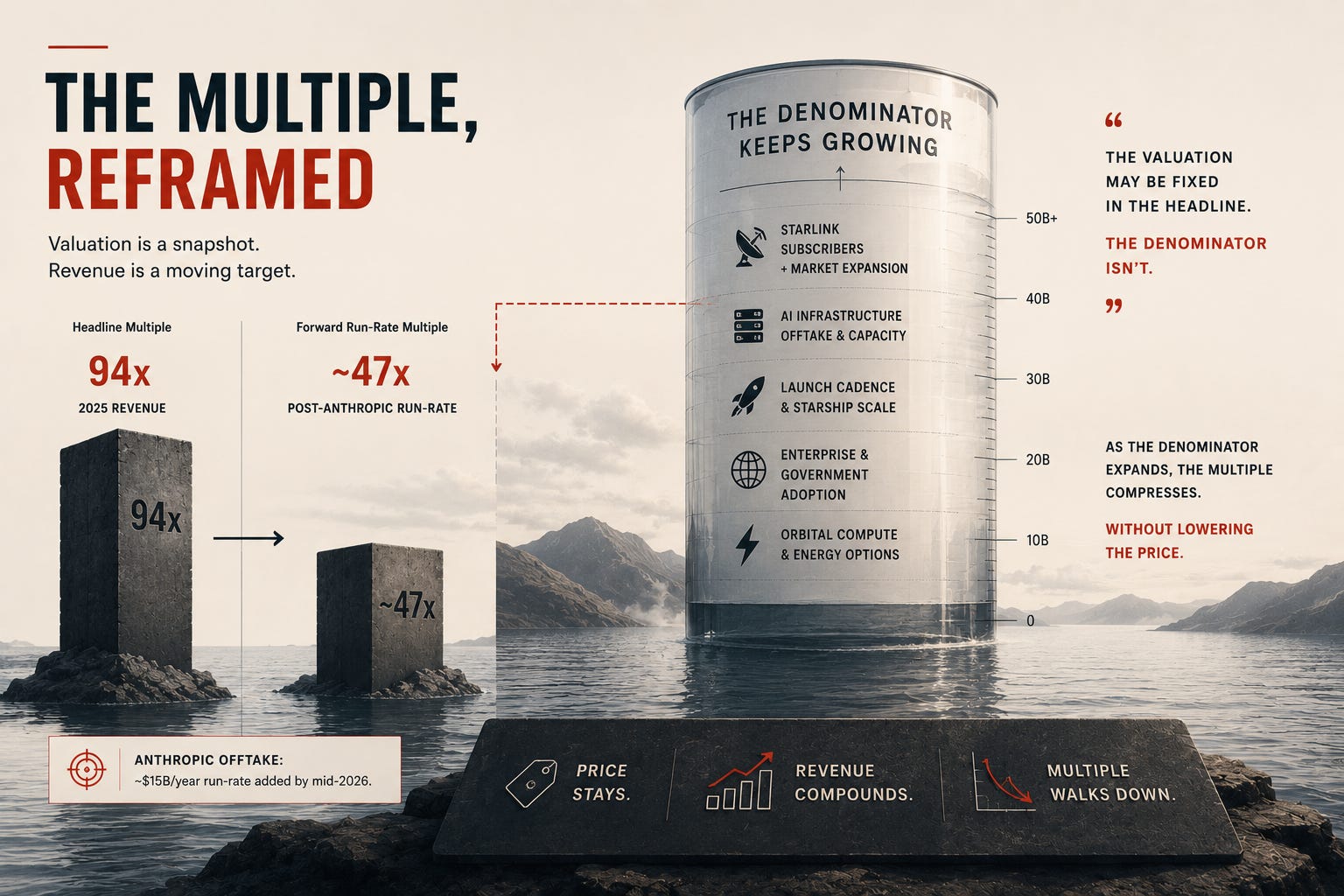

Before getting to the test itself, I want to sit with the 94x number for a moment because it’s the number that does the most work in the bear case, and I think it’s also the most misunderstood.

The 94x is calculated on 2025 revenue. SpaceX 2025 revenue is, mechanically, the past. The Anthropic-Colossus offtake is $1.25B per month, $15B per year, north of $40B contracted through 2029, which is essentially zero in the 2025 number and effectively a full year of run-rate by mid-2026.

If you take a more conservative post-listing valuation of $1.5T and overlay the Anthropic-annualized revenue, you’re closer to ~47x on a forward run-rate basis. Still rich. But a very different conversation than 94x.

Now compare across the AI-infra premium tier. Cursor’s potential $60B acquisition offer from SpaceX on roughly $2B ARR, with $6B forward ARR projected by year-end, somewhere in the 10-30x revenue range depending on how forward you go.

Cursor is software-only and is being valued by growth investors on a forward basis. If a code editor at $2B ARR clears 30x current, an orbital connectivity utility + launch monopoly + AI infrastructure stack at $20B run-rate clearing ~47x forward is not absurd.

There is a layer to this that also points to the xAI/SpaceX teams in being able to spin up a data center (or even a Starlink fab plant) at a speed and scale others in the industry haven’t delivered in the past. Nvidia CEO Jensen Huang famously praised Elon Musk’s construction of the xAI Colossus supercomputer (initially a 100,000-GPU cluster) as “superhuman,” noting it took just 19 days to get the first servers running workloads and 122 days for the initial full build… a feat that normally takes other companies four years. (Just this internal capability to spin up data center capacity at the speeds Anthropic and the AI market growth demand, is itself a skill/experience MOAT that can grow a whole new industry/revenue arm that has nothing to do with the space-play alpha that SpaceX dominates).

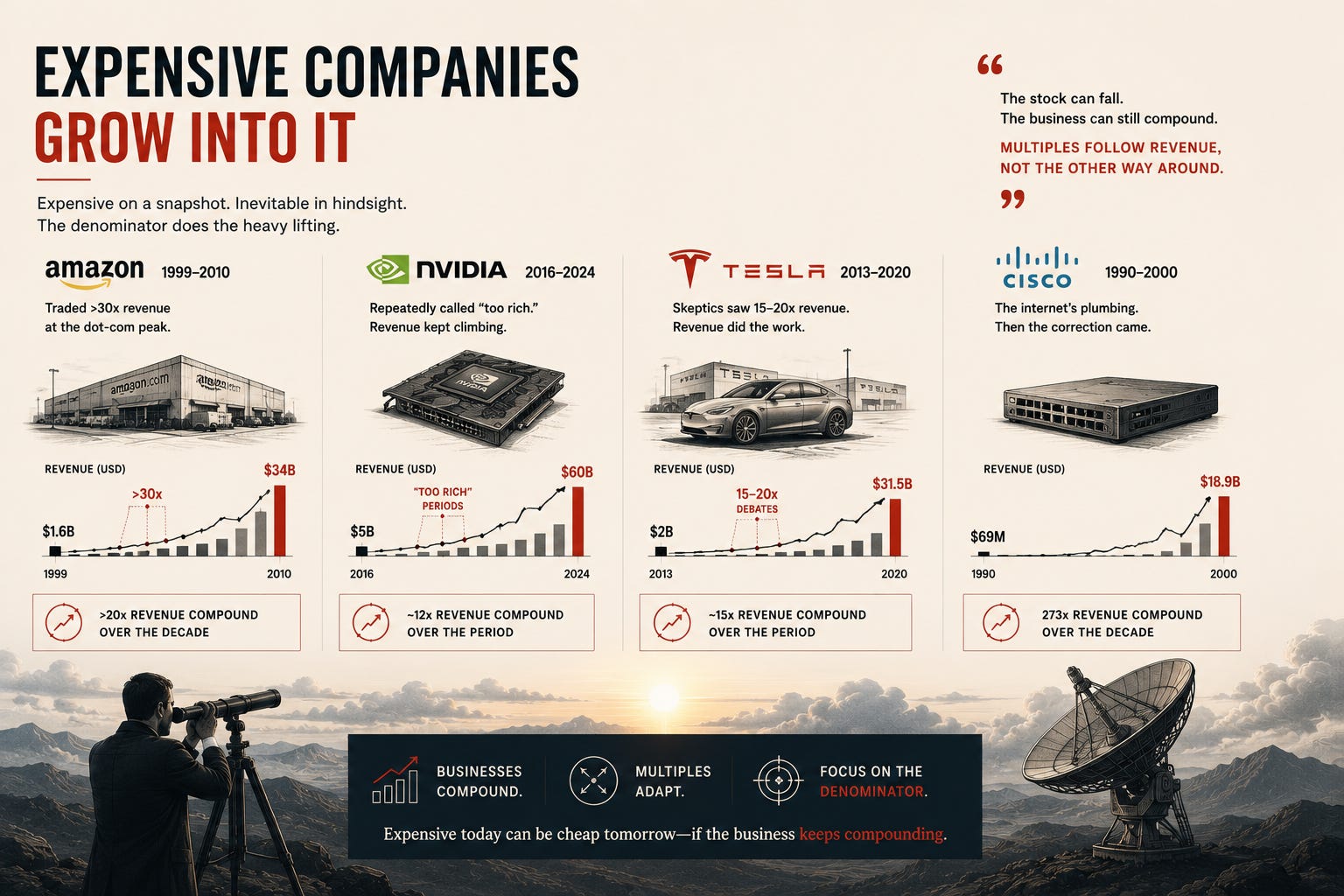

What gets missed in the 94x discourse is what’s actually historically rare about expensive companies… they almost always grow into the multiple rather than have it compressed down to them.

A few worth remembering:

Amazon, 1999–2010: traded north of 30x revenue at the dot-com peak. The stock collapsed. The company didn’t. Revenue went from $1.6B to $34B over the decade… a >20x revenue compound. The “expensive on revenue” company became the cheapest infrastructure asset on the public market because the denominator did the heavy lifting.

NVIDIA, 2016–2024: I bought NVDA in 2016 at a cost basis of ~$1.51 (post-split), as I wrote in Why Being Late. Through that period, the company traded at “too rich” P/S multiples repeatedly. Revenue compounded from ~$5B to ~$60B… 12x… while the stock did much more. The multiple compressed and the price ran. Both happened.

Tesla, 2013–2020: skeptics screamed about 15-20x revenue valuations every other quarter. Revenue went from $2B to $31.5B. The multiple compressed by way of denominator growth, not equity decline.

Cisco, 1990–2000: the internet’s plumbing went from $69M in revenue to $18.9B over the decade, a 273x revenue compound. Even after the 2000 correction, the business had compounded the entire decade. (The cautionary lesson there is what happens when an expensive multiple meets a slowing compound… relevant, but not the case for SpaceX in 2026.)

The point isn’t that expensive always works. It’s that for a category-defining infrastructure leader at the beginning of a structural compound, not the end, the revenue multiple is a snapshot of a moving denominator. The denominator is what changes the picture, and the denominator is what compounds.

Now let’s do the actual math on the compound. Elon’s personal wealth has compounded at roughly 50% per year since 2012 by the public estimates, that’s the empirical track record across Tesla, SpaceX and now xAI.

If you extend that same compound to SpaceX revenue and just halve it to a much more conservative ~25% growth assumption, SpaceX gets to ~$25B in 2026 from $18.6B in 2025. Layer the Anthropic deal on top and you’re at $40B run-rate. That’s a 2x revenue compound in twelve months, without a single new contract beyond what’s already announced. The 94x quietly walks itself down to the mid-40s before anyone touches the stock price.

And the war chest is the part that should make a bear pause. SpaceX has $15.9B in cash today. The IPO is targeting up to $75B of fresh primary capital. That’s a ~$90B war chest going into a moment where the entire AI infrastructure market is supply-constrained, terrestrial data centers are running into siting and grid limits and SpaceX is the only operator on Earth that controls every layer from launch to compute to connectivity.

You don’t need genius capital allocation in that setup. You need one more Anthropic-sized offtake, for another $15B/year contract from any of the obvious counterparties (and Anthropic itself has explicitly signaled appetite for more), to add another ~50% to run-rate revenue. Most of that $90B is going to data center capacity.

And if Starship-enabled orbital data centers actually unlock a structural cost advantage on AI compute: cooling, energy, land, latency-bounded workloads all rethought from the orbital side then this entire conversation about revenue multiples becomes the wrong conversation. That isn’t 47x compressing to 20x. That’s a category being redefined in a way that doesn’t have a clean comparable.

When the category gets redefined by the leader, the multiple stops being the right unit of measurement.

That’s the part of the trade I’m not selling.

What the S-1 confirmed about my original thesis

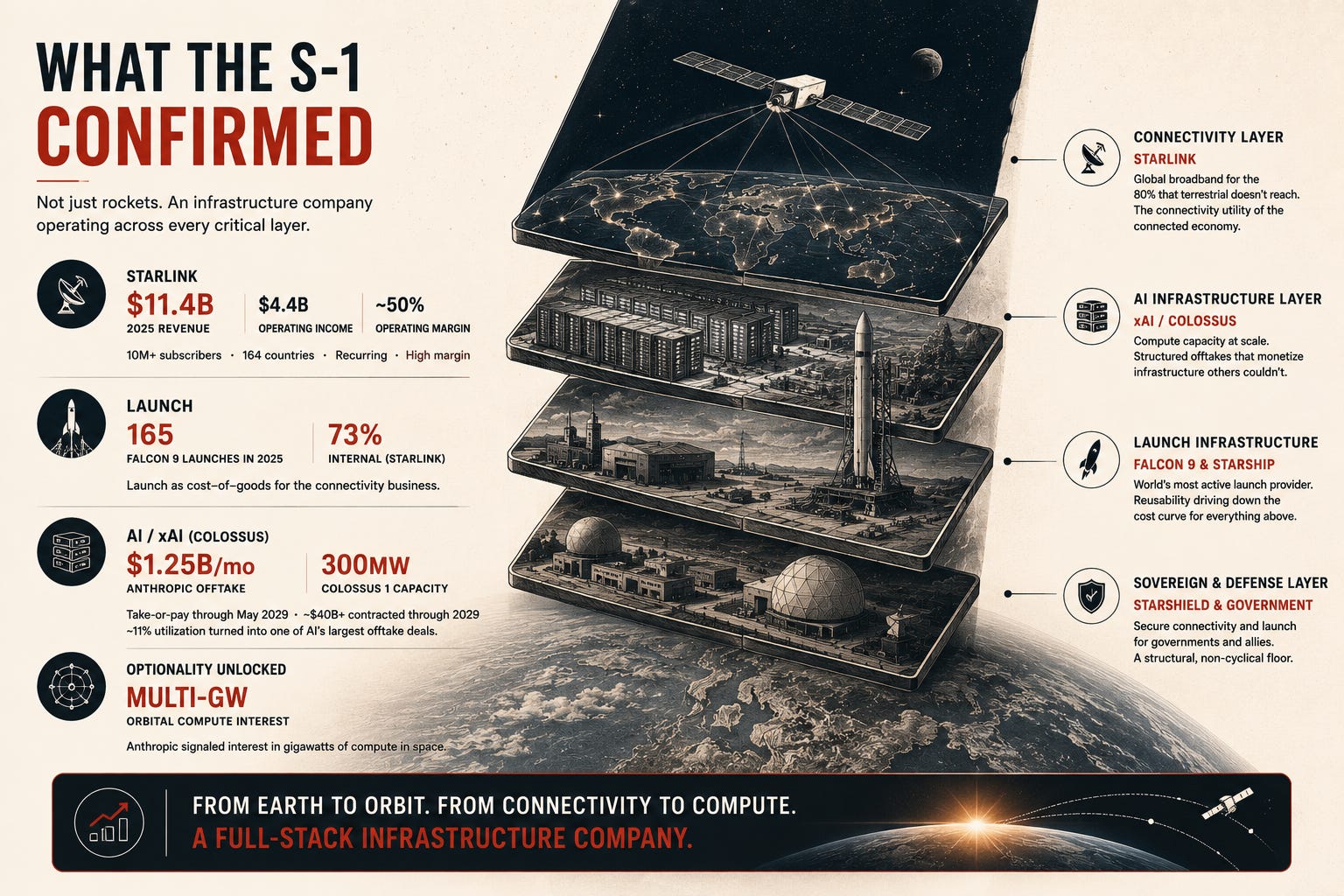

Two years ago, I wrote that someone has to build the communications infrastructure for the emerging space economy and that SpaceX had quietly achieved a near-monopoly on the first critical piece. The S-1 is the first time we get to see what that thesis looks like with audited numbers underneath it.

Starlink generated $11.4B in 2025 revenue, up nearly 50% year-over-year, with $4.4B in operating income, a ~50% operating margin business at scale. Over 10 million subscribers across 164 countries as of early 2026. This is no longer a satellite story. It’s a scaled, profitable, recurring connectivity utility and most of its addressable market lies on the ~80% of global land mass that terrestrial networks don’t reach.

The proof point I keep returning to is John Deere. Deere’s RFP for connectivity ran over a year. They tested 40 providers. They chose Starlink. Deere has 600,000 connected machines today, is targeting 1.5 million, and has a stated goal of fully autonomous farming systems by 2030. The S-1 names Deere directly as a flagship industrial customer. This is what the connected edge looks like when it actually arrives and it arrives through SpaceX.

The launch business is misread by the market. SpaceX ran 165 Falcon 9 launches in 2025; only 43 were for outside customers. Nearly three-quarters of all launches were internal, they were Starlink. The launch business isn’t underperforming, as the 8% YoY growth suggests on the surface. It’s being run as cost-of-goods for the connectivity business.

The AI segment, via the xAI merger, is where the losses concentrate. It’s also where new optionality showed up that I had not underwritten when I originally invested. Earlier this month, Anthropic signed an agreement to take the full 300MW of compute capacity at Colossus 1 in Memphis, over 220,000 Nvidia GPUs, at approximately $1.25 billion per month through May 2029. That’s north of $40 billion of contracted revenue from a single offtake, on a data center that xAI was reportedly running at ~11% utilization. They turned a stranded compute asset into one of the largest take-or-pay style contracts the AI infrastructure build-out has produced. That is a structured-finance lesson, not a story about renting GPUs to a competitor.

Buried in the same announcement: Anthropic also expressed interest in working with SpaceX on multiple gigawatts of compute capacity in space.

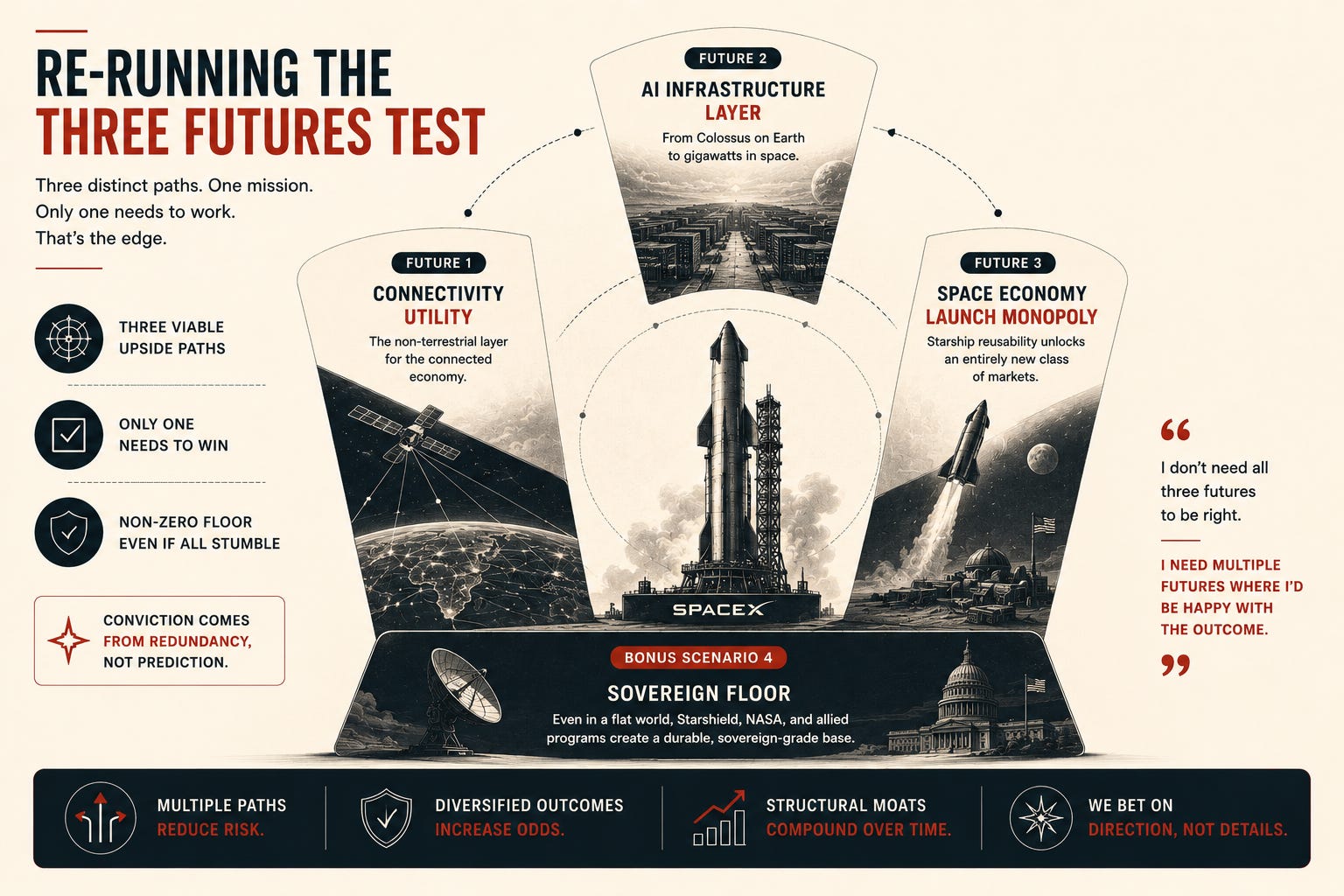

Re-running the Three Futures Test

When I originally invested, years before either of my write-ups existed, the three futures I could envision for SpaceX were: commercial satellite services, deeper space exploration and Mars cargo. As I wrote in the original piece, I didn’t need all three to work… I needed one. Starlink at 5–10% of the global telecom market was enough to justify the bet on its own.

With the S-1 now in front of me, here is how I’d re-run the Three Futures Test today:

Future 1 — Starlink becomes the connectivity utility for the connected economy. Not the consumer broadband product. The non-terrestrial layer underneath everything that operates outside the ~20% of land that terrestrial networks actually cover, agriculture (Deere), maritime (something I look at constantly through Fifth Wave), energy infrastructure, defense (Starshield), MRV-grade climate sensing, autonomous mobility. Recurring, contracted, high-margin with a moat that compounds with every satellite generation. A few hundred billion of the IPO valuation is defensible on Starlink alone.

Future 2 — SpaceX becomes the infrastructure layer of the AI compute build-out. The Anthropic-Colossus deal is the template, a multi-year, gigawatt-scale, take-or-pay style contract that monetizes infrastructure most operators were treating as a sunk capital problem. As terrestrial data center siting gets harder (the Memphis pollution fights around Colossus are the leading indicator, not the exception), the option value of gigawatts of orbital compute becomes a real conversation. Only one company controls the launch cost curve that makes that conversation possible.

Future 3 — The space economy itself matures, and SpaceX is the launch monopoly underneath all of it. Starship reusability economics, if they materialize anywhere close to targeted, change the unit cost of putting mass in orbit by an order of magnitude. That makes lunar cargo, in-space manufacturing, and the wildcard I personally find most underrated: Space-Based Solar Power, actually pencil. Caltech’s MAPLE demonstrator successfully beamed power from orbit to a receiver on Earth in 2023. JAXA and Mitsubishi have transmitted multi-kilowatt power across hundreds of meters on the ground. China is building dedicated SBSP testing infrastructure in Bishan and has publicly stated its ambition to deploy the first commercial space-based solar facility. The skeptics on SBSP are the same skeptics who told me Starlink wouldn’t scale past hobbyists. I’m willing to take that side of the trade again.

Bonus Scenario 4 — the devil’s advocate. Even if AI capex normalizes, even if the orbital compute conversation gets pushed to the 2030s, even if Starship execution slips by another five years… the floor under SpaceX is Starshield, NASA and allied sovereign space programs. Government dependency on SpaceX for launch and secure connectivity is now structural, not contractual. In a flatter, less euphoric future, the launch monopoly and the defense connectivity layer alone produce a durable, sovereign-grade revenue base. The pessimistic scenario doesn’t look like a zero. It looks like a slow compounder.

That’s the test. Three viable futures where I’d be happy with the outcome, only one of which needs to play out and a pessimistic fourth that doesn’t break the position even if all three of the others stumble.

Sizing the $5T scenario

Here’s where I want to push the framework one step further than I usually do because the question I keep getting asked by friends and LPs this week is some version of “sure, but where could this actually go?“ The $1.75T IPO is the floor case for the bull thesis. What I find more interesting is the next leg: what would have to be true for SpaceX to be a $5 trillion company?

The number sounds absurd until you do the unit math. At the mature-leader revenue multiples that NVIDIA, Microsoft, and Apple trade at (15-20x), $5T implies somewhere between $250-330B of annual revenue. SpaceX exits 2025 at $18.6B and arrives in 2026 at roughly $35B run-rate including the Anthropic deal annualized. So the question becomes: what does it take to compound from $35B to ~$300B over the next decade?

The thing about applying the Three Futures Test at this scale is that no single future has to do all the work. The same logic that made me comfortable buying SpaceX at $40B applies here… three viable paths, only one needs to land. So let me size each one.

Future 1: The connectivity utility. What does Starlink-as-galactic-telecom look like at the scale that moves the needle? Global telecom services is a ~$1.5 trillion market. Verizon, AT&T, China Mobile, and Deutsche Telekom each generate $120-140B in revenue at industry-standard 15-25% operating margins. Starlink already runs at 50% operating margins, roughly twice the industry. To do $150B in connectivity revenue, SpaceX would need to capture ~10% of the global telecom market, roughly the equivalent of becoming the world’s largest single telecom operator. Or, more accurately for the segment Starlink actually competes in: own the non-terrestrial layer underneath every connected machine on the 80% of land terrestrial networks don’t reach, plus maritime, plus aviation, plus defense, plus IoT/edge. That’s not displacing Verizon. That’s building the layer Verizon doesn’t have. One Verizon-equivalent of revenue at twice the margin is one path.

Two Verizon-equivalents, at this margin profile, is most of the way to $5T on connectivity alone.

Future 2: The launch-monopoly-times-space-economy. This is the future that depends entirely on Starship economics. If reusability hits anywhere close to targeted unit cost, say $200-500/kg to LEO from current $1,500-3,000/kg, every existing market for space-based services repriced down by an order of magnitude becomes a new addressable market. Earth observation, in-space manufacturing, lunar logistics, defense constellations, Mars cargo, none individually a huge revenue line today, but collectively a category that doesn’t yet exist as a financial market.

To do $50-75B in launch + adjacent space services revenue, SpaceX needs to be the underlying infrastructure for roughly 80-90% of orbital activity over the next decade. They are already at 80%+ of global launch mass.

The harder question I ask isn’t whether they’ll dominate… it’s how big the category itself gets when launch stops being the bottleneck.

Future 3 (formerly the bonus): Becoming AI’s infrastructure utility — on land first, in space eventually. This is the one that surprised me when I worked through the math. The Anthropic-Colossus deal is $15B/year. AWS does $108B in cloud revenue. Azure does ~$80B. To become a top-3 AI compute provider by 2030, SpaceX would need to scale Colossus + sister facilities to 5-10 GW of deployed compute capacity, versus the current ~300 MW at Colossus 1. That’s roughly 5-10 more Anthropic-sized offtakes, against a hyperscaler capex pool that already exceeded $320B in 2025 and is forecast to clear $1T annually by 2030. The supply-side constraint is energy, land, water, and grid, exactly the bottlenecks SpaceX is uniquely positioned to route around. $100B in AI compute revenue by 2030 is not a stretch case. It’s roughly the trajectory the market is already underwriting for the existing hyperscalers, just transferred to a new operator with a structural moat the incumbents don’t have. And that’s all on Earth, before orbital compute enters the conversation.

The bonus option: Space-Based Solar Power. This is the wildcard I find most underrated and the hardest to size partly because the unit economics aren’t yet a financial market, and partly because the engineering trajectory is steepest. For context: 1 GW of continuous baseload generates ~8.76 TWh/year; premium clean firm power for data centers and industrial loads can clear $80-150/MWh. To do $50B in SBSP revenue at the premium end, SpaceX would need to deliver ~40-50 GW of continuous power-beamed capacity, roughly half the entire US installed nuclear fleet, beamed from orbit. That is a 10-15 year engineering ramp from where Caltech’s MAPLE demonstrator sits today. I’m not underwriting this as part of the base case. But it’s the only one of the four where the category itself gets redefined and where the structural cost advantage I keep referring to lives. If it works, it’s not a $50B line item. It’s the energy backbone for AI compute, and the multiple stops being the right framing entirely.

Blending the futures. Here’s the part the spreadsheet wants me to say out loud: I don’t need any one of these to fully play out to get to $5T.

A blended scenario looks something like — $150B connectivity + $50B launch/space services + $75B compute + $25B optional SBSP/other = $300B revenue at 15-20x = $4.5-6T.

That blend doesn’t require Starlink to displace Verizon, doesn’t require Starship to deliver Mars cargo by 2030, doesn’t require any of the more aggressive single-path assumptions.

It just requires each of the three futures to land somewhere between 30-60% of its ceiling. Which is, structurally, what the Three Futures Test is actually testing for. You don’t need any one bet to hit the moon. You need three bets where the floor of each is meaningful and the ceiling of any one is enormous.

The question I’d encourage anyone reading the S-1 to ask isn’t “is $5T possible?“ — it’s “which of these three paths am I willing to bet against simultaneously?“ Because that’s what shorting SpaceX from here implicitly does.

You have to be wrong on connectivity, wrong on launch economics, and wrong on AI infrastructure and also right that SBSP never materializes over a ten-year window where SpaceX has a $90B war chest, controls the launch cost curve and is the only operator that can actually run the experiment.

I’m not willing to take the other side of that trade.

SpaceX Flywheel in Motion: Where Market Structure Meets the Long View

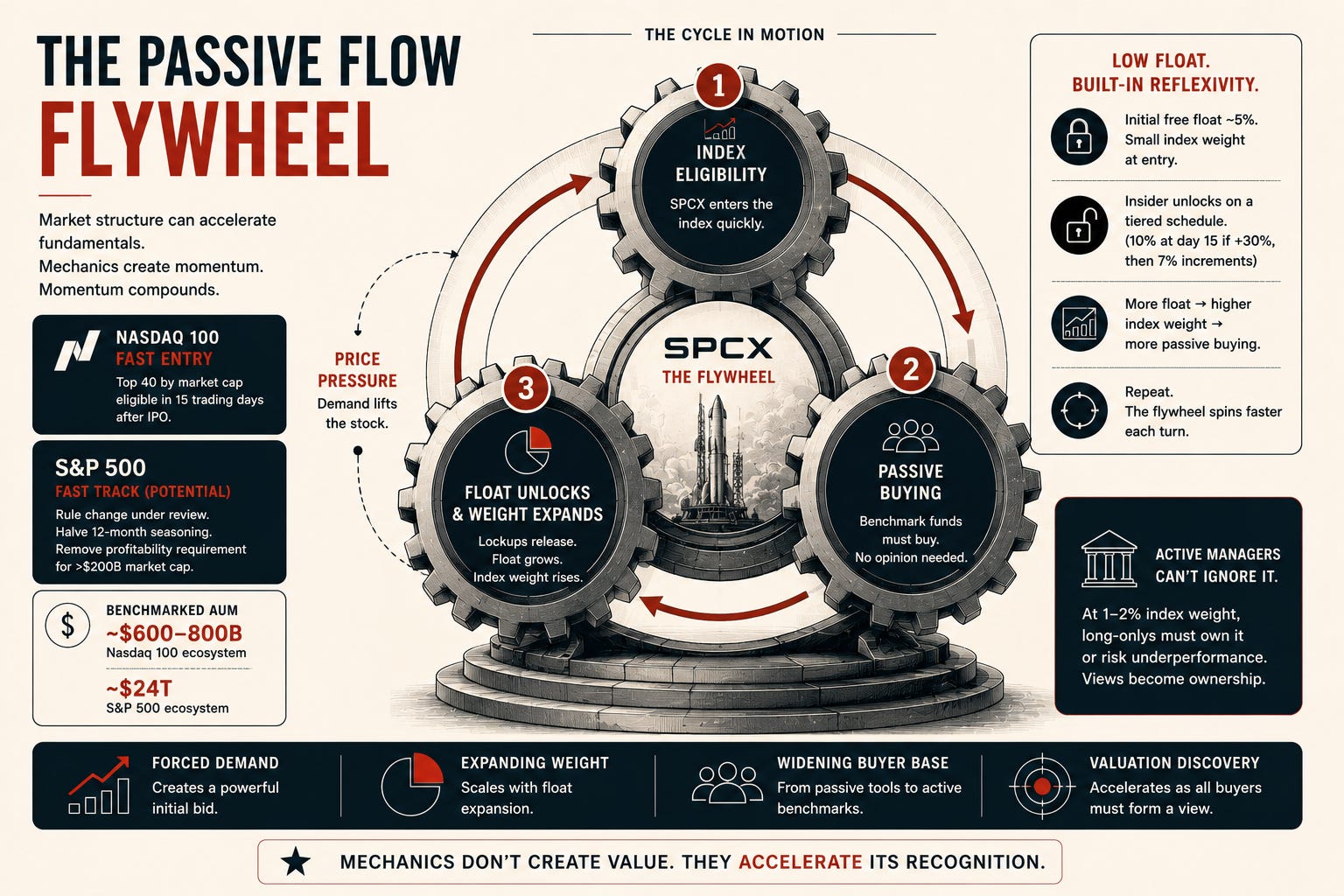

There’s one more piece I want to put on the table, because if you spent any time watching $INTC over the last year you’ll already be familiar with the convention, the 🚩 flag for the largest asset allocators, when the market structure itself is about to do most of the work, separate from any fundamental view.

There are two unique mechanics around SPCX that I think most retail commentary is dramatically underweighting.

The first is the Nasdaq 100 “Fast Entry” rule, which went into effect on May 1, 2026. Under the new framework, companies whose market cap ranks within the top 40 of the index become eligible for inclusion just 15 trading days after IPO, down from a historic seasoning period of three to twelve months. SPCX at $1.75T will sail through that threshold. The Nasdaq 100 is tracked by roughly $600-800B in passive AUM across QQQ, QQQM, and the broader NDX-tracking mutual fund and institutional mandate universe. Inclusion forces all of them to take a benchmark-weight position within days, regardless of any view on the multiple, the lockup structure, or the underlying fundamentals.

The mechanic that makes this especially interesting is the low-float weighting that scales as float expands. SPCX is going to enter the index with a small free float, somewhere around 5%, which means a fractional initial weighting. But the insider lockup releases on a tiered schedule: 10% of insider shares unlock at day 15 if the stock is 30% above IPO, then 7% increments at days 70, 90, 105, 120, and 135. Each unlock expands float, which scales index weight, which triggers more forced passive buying. This is reflexivity engineered directly into the listing structure.

First passive bid lifts the stock through the unlock trigger → more float comes online → index weight rises → the next passive bid is larger. Each turn of the flywheel widens the AUM pool that has to chase.

The second mechanic, and the bigger one, is the S&P 500 rule change that’s under active consideration right now. S&P Dow Jones Indices opened a formal review in March of whether to fast-track mega-cap IPOs into the S&P 500, specifically halving the 12-month seasoning period and eliminating the GAAP profitability requirement for companies with market caps above $200B. The consultation period closes May 28. Changes could take effect June 8. The SPCX listing is targeted for June 12. The timing is not a coincidence.

If the rule passes in time, the consequences scale up by roughly an order of magnitude.

The S&P 500 has roughly $24 trillion in benchmarked AUM, about 30x the Nasdaq 100 pool. The forced passive buying alone would be a step-change. But the more important effect is on the active side: long-only managers benchmarked to the S&P 500 cannot stay underweight a 1-2% index name without taking real career risk. If SPCX enters at ~$1.75T (~0.5% of total S&P market cap) and runs toward $3T+ over the next 12-18 months on fundamentals, it becomes a 1-2% weight that every benchmark-aware active manager has to have a view on. Long-onlys will be forced to take a view. And that view, for most of them, will be some version of “we have to own at least benchmark weight.” Independent of fundamental conviction.

The combined effect of both rule changes, Nasdaq fast-entry plus S&P fast-track, is that the natural compounding I described in the multiples section gets a turbocharge from passive flows and forced active positioning. The multiple compression doesn’t have to wait for revenue to fully catch up. The buyer base catches up first.

Now, the honest version of this story includes the critics. Michael Burry has flagged the proposed changes publicly. George Noble called them a “shameless” manipulation of index methodology, arguing the traditional seasoning periods exist for a reason: they allow real price discovery and protect passive investors from being forced into untested, illiquid securities. I take that critique seriously. In any other moment, I’d be sympathetic to it.

But here’s the part that, for me, reframes the whole conversation: the only reason index providers are even contemplating these rule changes is that the existing rules cannot accommodate a generation of category-defining companies that stayed private at extraordinary scale. SpaceX, OpenAI, Anthropic… their market caps already exceed 95% of current index constituents before they list. The rules were designed for a world where companies IPO’d at $1-10B and grew into mega-cap status over decades. They don’t work for companies that arrive on the public market already at $1T+. The mechanics being engineered now are downstream of a structural reality: the private market kept these companies inaccessible to public-market investors for a generation. The rule changes are, in some sense, the public market catching up to the private one.

For me as a long-term holder, the index mechanics aren’t the reason to hold SpaceX, the Three Futures Test is the reason. But the mechanics do something important: they accelerate the discovery of the real multiple. Once the entire benchmark-aware active management complex has to have a view on SPCX, the public market valuation stops being a function of “what’s the smart money saying at this exact moment” and starts being a function of “what’s the structural floor of forced ownership at this benchmark weight.” That floor is what lets long-term holders like me stop checking the chart on any given day.

100% this is financial engineering and it’s worth saying that part out loud. But the engineering is structurally aligned with the long-view investment philosophy I’ve been running for a decade. When the index becomes the dominant buyer of a category-defining business, the daily volatility becomes noise around a slowly-rising benchmark-weighted floor. That is exactly the kind of structural setup that lets me do what I do best: sit still and let direction compound.

What I’m doing

I’m holding and specifically holding for the part of the return I haven’t earned yet.

The plan is to keep a meaningful core position for the next decade and revisit sizing thoughtfully over time. Not because I think the multiple is wrong, but because position-sizing discipline eventually matters more than directional conviction at this scale. Trimming because a position got large is a different question from whether the thesis still holds, in my opinion, the thesis still holds.

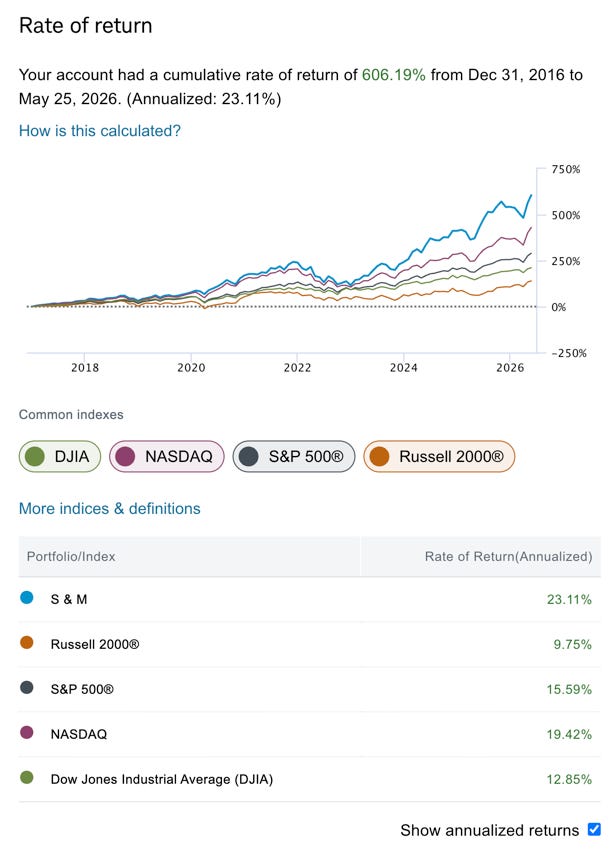

When I look back at my own public-market returns over the decade, 606.19% cumulative, 23.11% annualized, well ahead of the S&P 500 (15.59%), NASDAQ (19.42%), DJIA (12.85%), and Russell 2000 (9.75%) over the same window, almost none of that came from timing. It came from being directionally right and being still. The years where the spread between my portfolio and the indices opened up the widest were the years I did the least.

Personal public-market portfolio vs. major U.S. indices, Dec 31, 2016 – May 25, 2026. Source: Charles Schwab. 23.11% annualized over the past decade.

My own Schwab account return over the same period is less interesting to me as a scoreboard than as evidence of the behavior the essay is really about: being directionally right, sizing risk, and sitting still.

SpaceX, for me, is the most concentrated expression of that philosophy I’ve ever put on. A direction I bought into a decade ago, that’s about to become a public-market ticker, that, by my honest read of the S-1, still has most of its compound ahead of it. The trade isn’t to exit at the IPO. The trade is to keep doing what’s already worked: stay directional, stay still, and let the compound do the work.

Closing Thought

The 94x multiple is, at its core, a question about whether you’re paying for the past or the future. If you’re underwriting SpaceX on 2025 financials, the answer is obvious and you should pass. If you’re underwriting the connectivity layer of the connected economy, the structured offtake of AI infrastructure, and the Starship-enabled space economy, with orbital compute and power beaming sitting on top as call options, you stay in the seat.

When I wrote Why Being Late, the point was simple: when you can see multiple futures where you’d be happy with the outcome, the pressure of timing fades away. SpaceX is the cleanest example I have of that thesis playing out in my own portfolio.

I bought a direction, years before I ever sat down to write about it. A year and a half after I did write it down, and one S-1 later, that direction is more confirmed than I imagined at the time. The ticker and access is changing but my core thesis hasn’t.

In my view, there’s still 90% (or equivalently large %) of the journey ahead.